The Economy In Denial: Fallout from the Bursting Housing Bubble

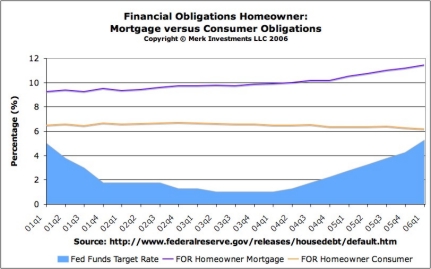

Axel Merk, Sep 21st 2006 Every day, another economist claims that the impact of the slowdown in housing on the economy is overrated; a few months ago, many still disputed there even was a housing bubble. There has been a housing bubble, the bubble has only started to deflate, and it may have very negative long-term implications for the US economy as well as the US dollar. Almost every day, a high profile company directly or indirectly targeting the US consumer warns that its outlook is bleak. Let it be Yahoo warning about advertising revenues; let it be Kellogg’s warning about its high costs; let it be Dell’s warning that its eternal rebate programs cannot push sales anymore; let it be the automakers that sell many of their brands at prices below last year’s level, yet are still unable to boost volume. All these incidents are linked to the US consumer; and US consumer spending, in turn is very closely linked to the health in the housing market. It also comes as no surprise that so far this year, the US dollar has fallen significantly versus a basket of currencies. Home building activity has collapsed with some builders reporting as many as half their orders cancelled. The volume of homes sold has declined and inventories are up. Home prices have – so far - held up reasonably well mostly because the cost of long term mortgages has been very well behaved; while short-term interest rates have risen, interest rates on longer term loans have in some instances even come down. As a result, the squeeze on consumer spending has been relatively mild and limited to a squeeze on home owners who have been dependent on adjustable rate mortgages who have seen their rates rise; beyond that, the squeeze has been on home owners who have employed their homes as ATM machines – these owners are dependent on eternally rising home values to finance their spending. By keeping inflation expectations low and the threat of an economic slowdown high, the Federal Reserve (Fed) has engineered an environment where home owners have the opportunity to move out of adjustable rate mortgages into longer-term, fixed-rate mortgages. The Fed publishes a “Financial Obligations Ratio” (FOR) that tries to capture all forms of debt service payments from lease payments on cars and other debt service payments such as mortgage payments as a percentage of disposable income. Please have a look at the chart that shows that breaks this ratio into debt service payments due to mortgage payments and those due to other consumer spending (the total Financial Obligations Ratio would be the sum of the two, not shown); the charts also shows the Fed Funds Target Rate, which the target interest rate the Fed charges other institutions for overnight lending. At the time of this writing, data have only been published through the end of the first quarter of 2006:

Now look on the right hand side of the graph, and you see that as interest rates creep up, the percentage of income spent to service mortgages has been going up. Aside from higher interest rates, home values continued to rise during this period. Because housing has held up reasonably well, we so far experience the “soft landing” scenario so many have been praying for. We often emphasize how dependent the US economy is on consumer spending. Economist Kurt Richebacher put this in perspective: "In 2005, real disposable incomes of private households in the United States increased $93.8 billion, or 1.2%, while their debts grew $1,208.6 billion, or 11.7%. Total consumer spending on goods, services and new housing accounted for 92% of real GDP growth." Unlike the stock market, the housing market is far less liquid; as a result, the unwinding of the housing bubble takes years. The “wealth effect” – the impact paper profits have on household spending – is far more significant in the housing market than it is in the stock market. The conclusion to draw is that we are in for a long and grinding road ahead. Let us tie in the dollar to the discussion. The boosting of household spending through low interest rates and low taxes has left its marks; the trade and current account deficits have soared, the dollar has not fared well:

We believe that we have only seen the beginning of the fallout of a slowing housing market. As inventories of unsold homes increase, home prices are likely to come down significantly in many parts of the country. Because consumers have so much more debt outstanding than in past economic cycles, the drag on economic activity will be amplified. In the meantime, we see the financial services sector engaging in more speculative activity. Blue chip firms are acquiring sub-prime mortgage lenders, such as Merrill Lynch paying $1.3 billion earlier this month to get $7 billion worth of risky loans onto their balance sheet. Merrill would refuse managing the savings of the mortgage holders, but is gladly taking on their debt; in an environment where just about everyone could get a mortgage, you must be in rather bad financial shape to resort to apply for a mortgage with a sub-prime lender. This particular lender Merrill acquired, the nation’s 10th largest, issued almost $30 billion in mortgages last year. The attraction in the business is the securitization of the mortgages into collateralized mortgage obligations (CMO’s) and the resulting segmentation into various securities. It is an open secret, however, that this is a very obscure market dealing in at times, very risky products that may not be well understood, sometimes not even by the issuer. In our view, just as investment banks are eager to load up their balance sheet with hot potatoes, a scandal waiting to happen is building in the mortgage industry. To make home ownership more accessible, many sub-prime lenders have offered mortgages where only a fraction of the interest is paid each month, and the remaining interest is rolled into the principal. In other words, each month, your mortgage is growing; the hope is that higher home values will bail the homeowner and the bank out. Needless to say, the holders of such mortgages typically make little or no deposit. Why do lenders get engaged in this sort of activity? Partially because the promised yield is attractive and these hot potatoes can be passed on. But, and here is the scandal, the bank can also record the full interest income each month, even if the homeowner only pays a fraction; because it is part of the terms of the mortgage that the homeowner only pays a fraction of the full interest, the mortgage is considered to be in good standing and the full interest is recorded as income. Of course, the balance sheet of the bank deteriorates, but as long as Wall Street is more focused on earnings than balance sheets, this is very attractive business. Some lenders are getting leery that the market may not play along forever. Washington Mutual, one of the largest financial institutions in the US and a major player in the adjustable rate mortgage market, recently opted to issue 20 billion euro (about USD 25.4 billion) of debt in Europe; Europe has a long tradition with large “secured debt” offerings, where mortgages are packaged for resale; continental Europe has not seen the distortions that have been created in the US housing market. We would not be surprised if there was one day a rude awakening that risks in these products may be higher than anticipated. Even if long-term interest rates remain low, it may well spell trouble for a growing number of homeowners. For homeowners to refinance, their homes need to be re-appraised. With a lot of arm twisting, appraisers gave their nod of approval, so that homeowners could get access to a mortgage. But there comes a point when home values decline that appraisers simply cannot endorse unreasonable home valuations anymore. At that point, homeowners are stuck with their current mortgage, possibly an adjustable rate mortgage. Homeowners may also not be able to afford to move away as selling their homes would not cover the mortgage. In an era where too many homeowners have opted to pay no money down, have closing costs rolled into the mortgage and likely even taken out an equity line of credit to finance the remodeling, this affects many homeowners. There are those who say there is nothing to worry about because there is a large group of homeowners with fixed rate mortgages with stable incomes. Prices are not set by those who do not sell; prices are set by supply and demand. And supply has been increasing, providing pressure on home values. When Treasury Secretary Paulson says that we must help the Chinese master their growth as it would be to our peril not to do so, what he means is that we cannot afford a slowdown. If we were suddenly to turn the US into a nation of savers (rather than consumers of imported goods), we could expect the dollar to recover. But because the housing market will have a worse impact on the economy than many anticipate, we expect the Fed to try to “rescue” the economy. With commodity prices coming down and long term interest rates falling, the fear of deflation is back on the table. Fed Chairman Bernanke is known to see grave dangers in deflation; before becoming Fed Chairman, he has commended Japan on its ultra-loose monetary policy; he has also written in-depth about the Great Depression and identified the gold standard and too strong a dollar as an impediment to an economic recovery. In conclusion, we see the housing market slowdown signal an upcoming recession. We see the dollar at risk should investments in the US decrease faster than consumption slows. And we see substantial risks to the dollar once it becomes apparent that the Fed will come to the perceived rescue of the economy. Even with gold under pressure in the short-term, investors in gold firmly believe that the Fed will have to opt for growth rather than price stability. As numerous asset classes may be at risk in the environment ahead, shifting money out of the dollar into a basket of hard currencies may provide valuable long-term diversification. We manage the Merk Hard Currency Fund, a fund that seeks to profit from a potential decline in the dollar. To learn more about the Fund, or to subscribe to our free newsletter, please visit www.merkfunds.com. Axel Merk The Merk Hard Currency Fund is a no-load mutual fund that invests in a basket of hard currencies from countries with strong monetary policies assembled to protect against the depreciation of the U.S. dollar relative to other currencies. The Fund may serve as a valuable diversification component as it seeks to protect against a decline in the dollar while potentially mitigating stock market, credit and interest risks—with the ease of investing in a mutual fund. The Fund may be appropriate for you if you are pursuing a long-term goal with a hard currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Fund and to download a prospectus, please visit www.merkfunds.com. The dollar chart above depicts the U.S. Dollar Index which is a trade-weighted geometric average of six currencies; the New York Board of Trade defines the Dollar Index; for specifications, please click here. The Dollar Index rises when the dollar increases in relation to the currencies the index tracks.It is not possible to invest directly in an index. Chart courtesy of www.stockcharts.com. Investors should consider the investment objectives, risks and charges and expenses of the Merk Hard Currency Fund carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Fund's website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest. The Fund primarily invests in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Fund owns and the price of the Fund’s shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Fund is subject to interest rate risk which is the risk that debt securities in the Fund’s portfolio will decline in value because of increases in market interest rates. As a non-diversified fund, the Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. The Fund may also invest in derivative securities which can be volatile and involve various types and degrees of risk. For a more complete discussion of these and other Fund risks please refer to the Fund’s prospectus. The views in this article were those of Axel Merk as of the newsletter's publication date and may not reflect his views at any time thereafter. These views and opinions should not be construed as investment advice nor considered as an offer to sell or a solicitation of an offer to buy shares of any securities mentioned herein. Mr. Merk is the founder and president of Merk Investments LLC and is the portfolio manager for the Merk Hard Currency Fund. Foreside Fund Services, LLC, distributor.

Thank you for your interest in the Merk perspective. To serve our audience better and to continue offering our insights free of charge, please enter your information below to continue reading.

|

|||||||||