International Equities: Currencies Matter

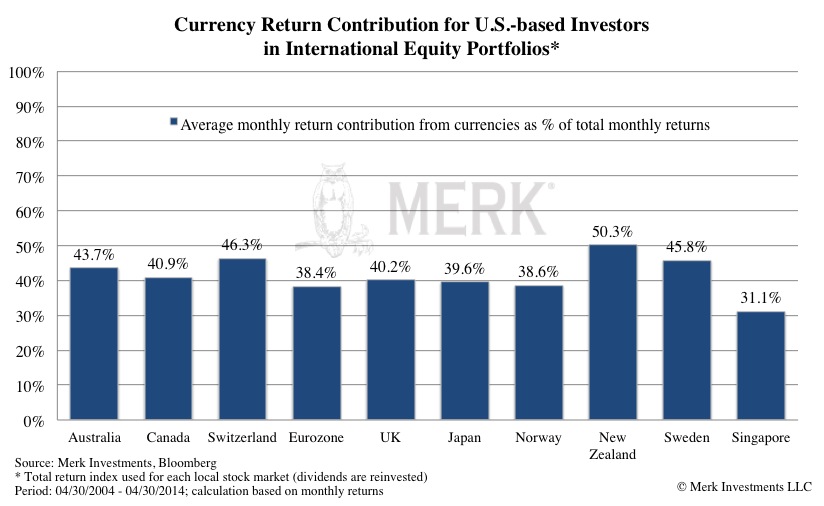

Axel Merk, Merk Investments May 8th, 2014 Hedging out the currency risk from international equities is currently en vogue after investors in the Japanese equity market dramatically enhanced their returns by hedging out the yen exposure in 2013. Market participants investing in international equities, must ask themselves: “to hedge or not to hedge?” As we shall elaborate, investors might be asking the wrong question. When investing in international equities, the return stream generated can be broken into equity returns and currency returns. As the chart below shows, between 30% and 50% of monthly equity index returns, when measured in U.S. dollars, were attributable to currency fluctuation1:

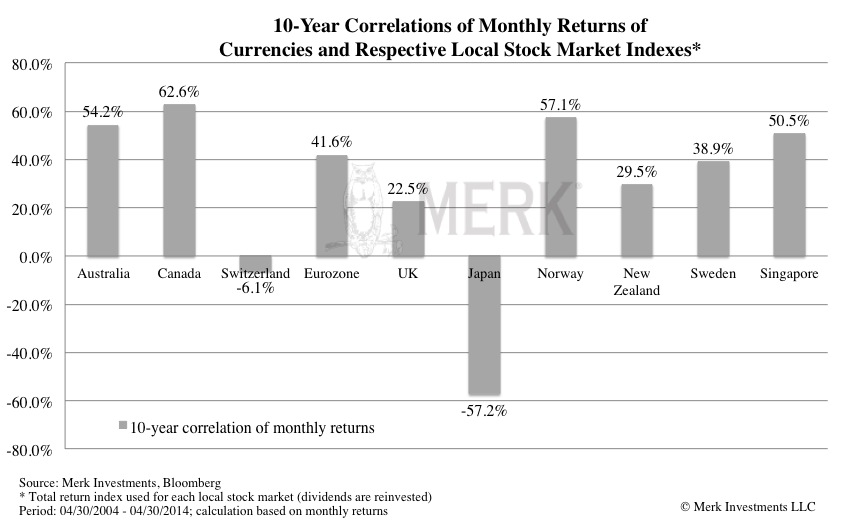

The contribution works on the upside, as well as on the downside. In a month where the local country’s stock market moved up, it is possible a good portion of the gain may be attributed to currency appreciation. Similarly, in a down month, a good portion of the loss may be attributed to currency depreciation. Let’s look at the correlation2 between the currency moves and these markets. For a currency-hedged international equity investment to enhance returns, one would want a rising equity market and a negative correlation between equities and the exchange rate:

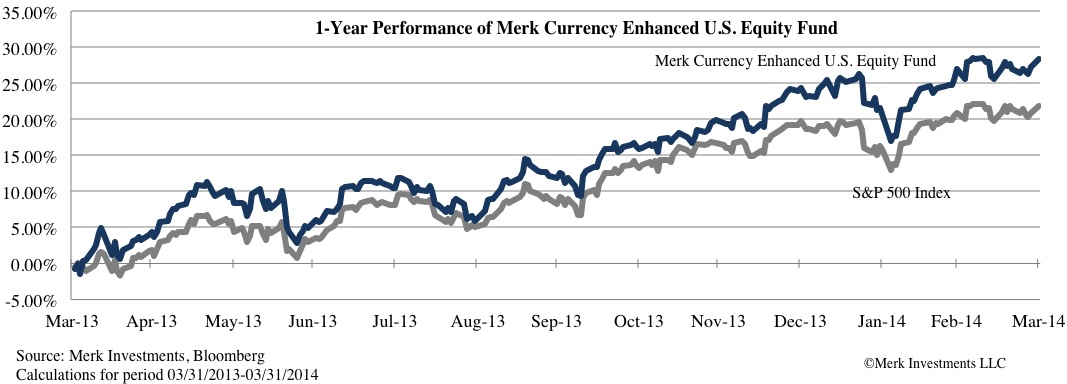

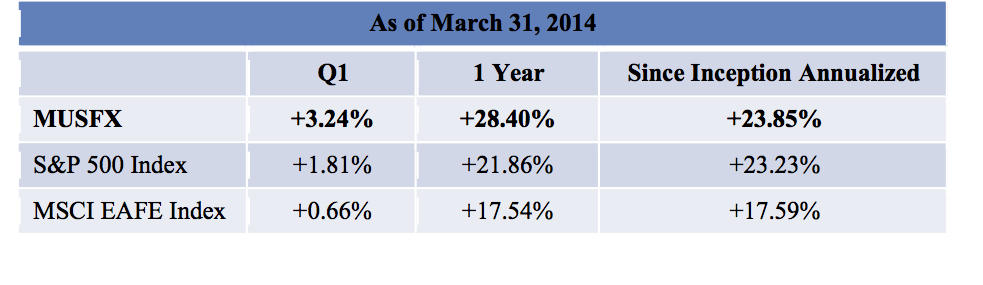

For currencies with positive correlation with the local stock market (e.g., euro), hedged investors may get a buffer when European stocks go down (by avoiding the double loss from both stocks and the euro), but lose the upside when European stocks go up (in which case the euro usually goes up). For currencies with negative correlation to the local stock market (e.g., Japanese yen), hedged investors may get higher returns when the Japanese stock market goes up (by avoiding the loss in the yen) but lose the buffer when Japanese stock market goes down (in which case the yen usually go up). If the yen continues to have a negative relationship with the Japanese stock market and the Nikkei rises, then it might make sense to hedge out the currency risk. However, note that this trade hasn’t worked well this year with a falling Nikkei and a rising yen. One of the reasons that investors may want to hedge the local currency exposure is because they feel they have an edge on making directional calls on broad equity markets in various countries but don’t understand the currency markets or don’t have a directional view on a given local currency. It would be frustrating to get the equity market call right and still lose money in U.S. dollar terms because of local currency fluctuation. Rather than hedging or not hedging, investors may want to consider actively managing currency risk. Not hedging and taking a leap of faith on up to half the returns on a return stream appears imprudent to us. But conversely, eliminating the potential value that currencies may bring provide can lead investors to leave returns on the table. What does it mean to actively hedge the currency risk? At risk of sounding self-promotional, this is what we do at Merk. We either zoom in on the currency risk, such as in our Merk Absolute Return Currency Fund (MABFX) where we trade in and out of currencies on either side of the dollar and possibly earn a modest rate on our collateral (i.e., no underlying equity exposure). In other words, the returns come primarily from the currency trading activity. In doing so, investors stay away from equity risk. But for those that have taken out the currency risk from their international equities through hedged international equity funds, we argue investors should consider managing the currency risk separately. The strategy pursued in MABFX is a “long/short” strategy, i.e., it does not have an ex-ante bias for or against the dollar. We can take a positive or negative position on any currency we invest in relative to the dollar at any time. To learn more, please download a fact sheet and read the prospectus. In our opinion, there’s no need to eliminate the currency risk for an equity investment. In our Merk Currency Enhanced U.S. Equity Fund (MUSFX), we are adding actively managed currency risk to U.S. equities with what is called a “currency overlay”. In doing so, the Fund adds a return stream that has historically had a low correlation with traditional asset classes and aims to generate positive active returns (i.e., alpha3). The Fund has beaten both the S&P 500 Index and the MSCI EAFE (an international equity benchmark) since inception:

Below is a visualization of the equity and currency components of the Merk Currency Enhanced U.S. Equity Fund (MUSFX). It is meant merely as an illustration of the concept of a currency overlay as described above.

The reason we mention this Fund here is to show that active currency management can add value to an equity portfolio. As this isn’t the place of extensively discuss this Fund, to learn more, please download a fact sheet and read the prospectus. To summarize: international investors may either be taking on unnecessary risk if they leave their foreign equity positions un-hedged from a currency standpoint, or they may be leaving attractive uncorrelated returns on the table by passively hedging. As a result we encourage investors to consider finding a way to actively managing currency risk. Don’t miss another Merk Insight: sign up for our free newsletter where we discuss how the U.S. dollar, gold and currencies impact investors’ portfolios. 1. Stock indexes used in this analysis: Australia: S&P/ASX 200 Net Total Return Index; Canada: S&P/TSX Composite Total Return Index; Switzerland: Swiss Market Gross Total Return Index; Eurozone: Euro Stoxx 50 Total Return Index; UK: FTSE 100 Total Return Index; Japan: Nikkei 225 Total Return Index; Norway: Oslo Stock Exchange OBX Index (It became a total return index since April 2006); New Zealand: NZX 50 Total Return Index; Sweden: OMX Stockholm 30 Total Return Index; Singapore: FTSE STI Total Return Index. All stock market indexes are in local currency terms and all include reinvested dividends. 2. Correlation is a statistical measure of how two securities move in relation to each other. 3. Alpha is a measure of risk-adjusted return. The excess return of the fund relative to the return of the benchmark is the fund’s alpha. S&P 500 Total Return Index (SPXT): a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. Performance figures assume that all dividends are reinvested. MSCI EAFE (Europe Australasia Far East) Index: a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. As international equity investment returns are a combination of equity returns and currency returns, the MSCI EAFE provides a useful comparison to a strategy including U.S. equities and currencies, like the Merk Currency Enhanced US Equity Fund. An investor cannot invest directly in an index.

Information contained herein may discuss Fund performance and holdings. Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than original cost. For performance current to the most recent month-end, please visit our website at www.merkfunds.com/fund. Through 3/31/22, the Merk Absolute Return Currency Fund Investor Shares (MABFX) had a 1-year return of , a 5-year return of , and a return of since inception on 09/09/2009; the Merk Hard Currency Fund Investor Shares (MERKX) had a 1-year return of -4.27%, a 5-year return of 0.07%, a 10-year-return of -2.1% and a return of 0.92% since inception on 5/10/2005. All performance figures greater than 1-year are annualized unless otherwise specified. The expense ratio for the Funds is 1.30%. In addition, these article excerpts and hyperlinks reference individual securities that may or may not currently be held by the Fund. Click here to view important information about the Funds, including their holdings. The views in these article excerpts and hyperlinks were those of the Fund's manager as of each article's publication date and may be subject to change.

Since the Funds primarily invest in foreign currencies, changes in currency exchange rates affect the value of what the Funds own and the price of the Funds’ shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, emerging market risk, and relatively illiquid markets. The Funds are subject to interest rate risk, which is the risk that debt securities in the Funds’ portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities, such as forward contracts, which can be volatile and involve various types and degrees of risk. If the U.S. dollar fluctuates in value against currencies the Funds are exposed to, your investment may also fluctuate in value. The Merk Currency Enhanced U.S. Equity Fund may invest in exchange traded funds (“ETFs”). Like stocks, ETFs are subject to fluctuations in market value, may trade at prices above or below net asset value and are subject to direct, as well as indirect fees and expenses. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. |