The End of Dollar Dominance?

Axel Merk, Merk Investments October 4, 2016 The end of U.S. dollar dominance may be unfolding in front of our eyes. No, we don't think China's ascent is the key threat; instead, key to understanding the U.S. dollar may be to understand the money market fund you might hold. Let me explain what's unfolding in front of our eyes, and what it might mean for the U.S. dollar and global markets.

Typically, when we think about potential threats to the dollar, we think a different reserve currency might take over; or that foreigners might dump their dollar holdings. I will touch on these, but then dive into what may be a much bigger elephant in the room. Bear with me.

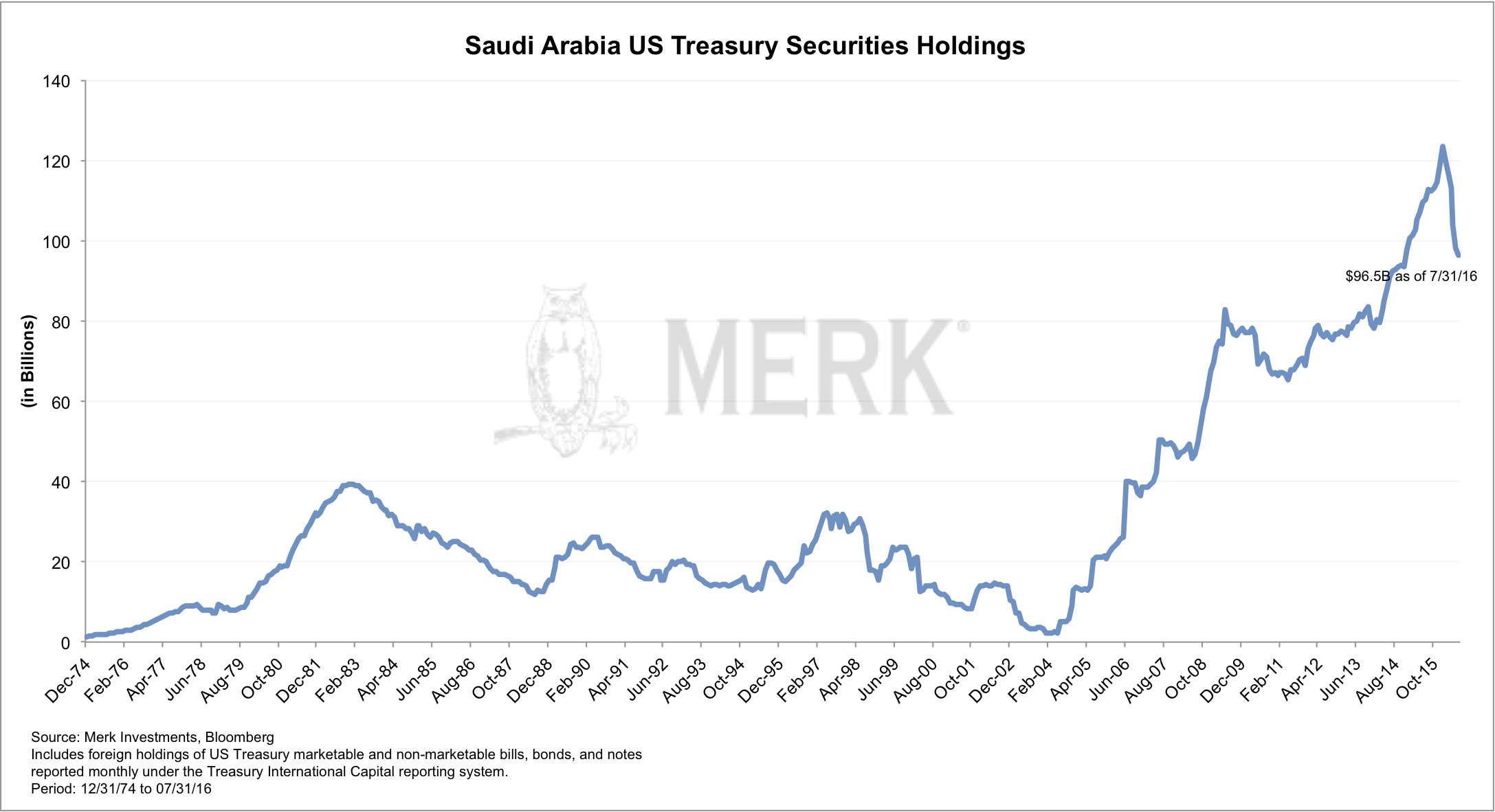

Foreigners holding U.S. debt That said, the recent decision by Congress to override President Obama's veto to allow private citizens to sue Saudi Arabia should get our attention. Saudi Arabia has threatened to sell its U.S. assets in case this law passes, as it doesn't want a judge to freeze their assets. As this chart below shows, this may not be an empty threat:

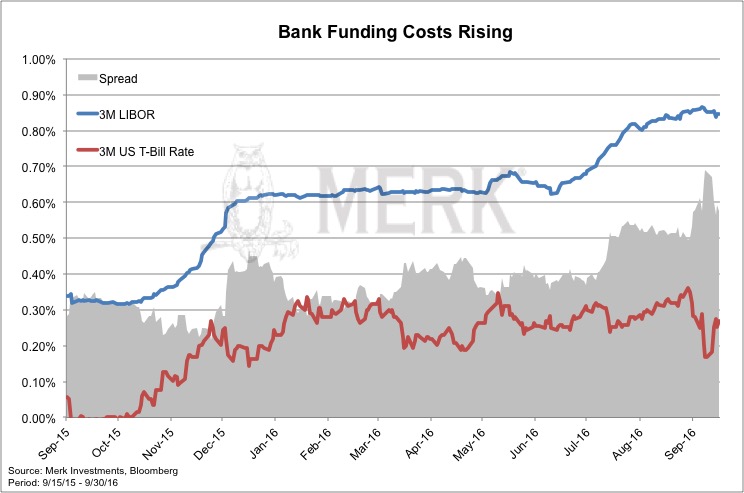

I write "may be" because there might be other reasons for the Saudis to sell U.S. Treasuries, such as a need to raise cash to deal with the fiscal challenges that have resulted from lower oil prices. Some say the inclusion of China's currency into the official basket of reserve currencies (SDRs) by the International Monetary Fund (IMF) is a clear sign that we have the beginning of the end of dollar dominance. In our assessment, this change is mostly symbolic. First of all, the new SDR basket barely changes the U.S. dollar weighting (other currencies were reduced to make space for the yuan); second, no large country manages its reserves according to the formula provided by the SDR; instead we allege that they manage them according to what they believe to be in their perceived self-interest. Where SDRs come into play is when the IMF provides a loan, as those are typically denominated in SDR. A belief in this theory suggests a great belief in the power of the IMF, an institution that has, ever since its inception, looked for reasons to be relevant. I'm not trying to discredit this theory, but am a firm believer that market forces playing out may well overwhelm the bureaucrats at the IMF for a long time. It turns out, though, that those that predict the end of the dollar dominance might still be right; not because of the IMF, though, but because of what we believe are massive changes underway in how anyone from foreign governments to foreign banks to foreign and domestic corporations fund themselves. Understanding Money Market Funds It turns out that this month, new rules for certain money market funds are being phased in. The regulations focus on institutional money market funds - you might not hold them in your retail brokerage account, but could be invested in one through your 401(k) plan. The new rules make it far less attractive for money market funds to invest in anything that's not U.S. government paper. Amongst others, institutional money market funds that invest in securities other than U.S. government paper must have a floating Net Asset Value rather than a fixed value of $1; they also must caution investors that their money might be held hostage for a few days in case of a panic in the market. Aside from a shift on how portfolio managers manage money market funds, investors are also thinking twice whether it's worthwhile to stuff money into money market funds when the returns are near zero, yet the risks are now higher (a floating NAV is riskier than a fixed one; so is the potential inability to withdraw money) than they used to be. As money market funds have been preparing for the new rules, we have seen seismic shifts in the world of global finance. Basically, until 2008, we believe there was a perception that money market funds were safe. The 'breaking of the buck' of a money market fund in 2008 threw cold water on that theory, but what few noticed is that it wasn't just an illusion for investors. For issuers of debt, it was what might be considered an implicit government guarantee (because the government set the rules on stable net asset value and liquidity), thus allowing issuers to access funding at what we believe was a subsidized rate. Think about it: a world where there's one place where funding is cheaper. Wouldn't you want to access that cheap pool of money if you were in need of cash? Well, you may not be large enough, but municipal and U.S. corporate issuers are large enough; so are foreign corporates, foreign banks and foreign sovereigns. If you have followed the markets since the financial crisis, you have probably heard of the LIBOR market. The U.S. dollar LIBOR rate reflects the cost of U.S. dollar funding outside of the U.S. It's a benchmark for anyone who isn't the U.S. government or a U.S. bank that can get financing from the Federal Reserve. If you look at this chart below, you will see that the funding cost has steadily been increasing:

In our assessment, the reason LIBOR has been increasing is because borrowers are no longer able to access U.S. money market funds as cheaply as they used to. With the new rules, I allege they have to pay closer to a true market rate rather than what used to be a subsidized rate. This doesn't just affect European banks, but also US corporate and municipal issuers. If you want to know why the Fed didn't raise rates in September, I believe the full phasing in of new money market fund rules is the main reason: the Fed wants to see how LIBOR rates behave. We believe this additional cost in the LIBOR market may well be permanent. And it may also be ultimately healthy for global markets, as borrowers will have to pay interest at a rate that's more reflective of their risk profile. However, that doesn't mean that there aren't major implications. End of Dollar Dominance? In today's world, though, a European bank is no longer able to tap into U.S. dollar funding at the same favorable terms, as evidenced by the higher LIBOR rates. That means their clients won't have access to the same embellished terms, either. Such clients may well decide to no longer seek a U.S. dollar loan, but instead a euro denominated loan, or a loan denominated in their home country's currency. This trend might be accelerated by the fact that interest rates in the Eurozone are lower than in the U.S. As much as we love to hate the euro, this trend may let the euro rise as a formidable competitor to the U.S. dollar as a reserve currency. What does it mean for the markets?To me, there is no question that this has massive implications for the markets. What implications, however, isn't quite as obvious. I'll mention a few here:

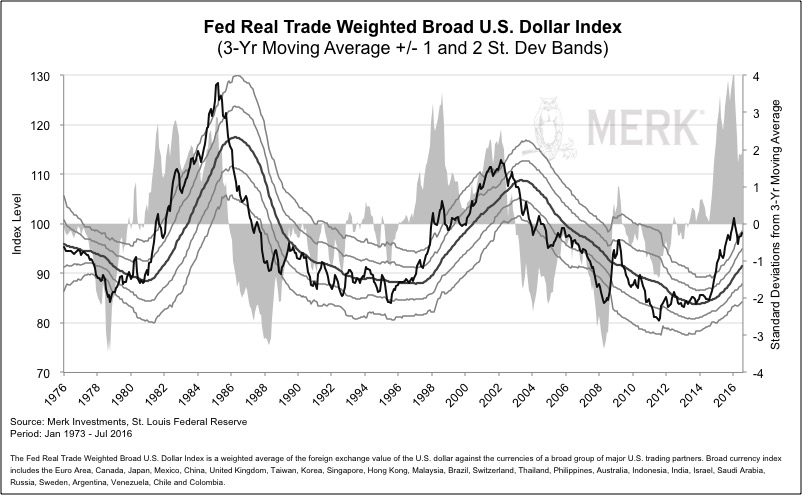

In the medium term, we expect funding in local currencies to increase. We have already said years ago that this will ultimately create a more stable global financial system. But it has ripple effects to the U.S. With global fixed income markets developing, U.S. fixed income markets might become less relevant. The Chinese government, for example, might not have as a much of a need to purchase U.S. Treasuries. That, in turn, might increase the borrowing cost for all U.S. borrowers, including the U.S. government. I use words like "may" and "might" not only because there are other scenarios. If I am not mistaken, for example, the U.S. cannot really afford much higher interest rates, especially if I look at the trajectory of U.S. deficits. As such, it's quite possible that the Federal Reserve may keep borrowing rates low. But I am a firm believer that there will be a valve; that valve may well be the U.S. dollar, which may decline in the process. Have I mentioned that we believe the U.S. dollar isn't exactly cheap right now? If you look at the chart below, you will see that we continue to be about two standard deviations above its longer-term moving average:

Some say that the dollar has to rise because U.S. rates may go up. In our analysis, real interest rates, i.e. those after inflation, may not go up as the Fed is at risk of falling further behind the curve; at the same time, interest rates in part of the rest of the world may have reached their lows. In this context, we see it is quite conceivable that the U.S. dollar could continue to weaken. Merk Hard Currency Fund A pitch for our hard return currency fund wouldn't be complete without a link to the fact sheet, prospectus and full attribution analysis. Please also register for our October 18 webinar with our quarterly update on our Funds and investment outlook. Also make sure you subscribe to our free Merk Insights, if you haven't already done so, and follow me at twitter.com/AxelMerk. If you believe this analysis might be of value to your friends, please share it with them. Axel Merk  Follow @AxelMerk Tweet Follow @AxelMerk Tweet

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments LLC makes no representation regarding the advisability of investing in the products herein. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice and is not intended as an endorsement of any specific investment. The information contained herein is general in nature and is provided solely for educational and informational purposes. The information provided does not constitute legal, financial or tax advice. You should obtain advice specific to your circumstances from your own legal, financial and tax advisors. Past performance is no guarantee of future results. Since the Fund primarily invests in foreign currencies, changes in currency exchange rates will affect the value of what the Fund owns and the price of the Funds shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Fund is subject to interest rate risk, which is the risk that debt securities in the Funds portfolio will decline in value because of increases in market interest rates. As a non-diversified fund, the Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. The Fund may also invest in derivative securities which can be volatile and involve various types and degrees of risk. In addition, the Fund is not a money market fund and therefore it does not seek to maintain a stable net asset value (NAV). For a more complete discussion of these and other Fund risks, please refer to the Funds prospectus. Before investing you should carefully consider the Fund's investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained by clicking here. Please read the prospectus carefully. Foreside Fund Services, LLC, distributor. Correlation: a measure of how two securities or asset classes move in relation to each other.

|